|

www.Finackle.com Home Mortgage Loan Mortgage Guide Step 4: Down Payments and Your Home Mortgage LoanWhy a Large Down Payments Saves You Money 1. Your Home Mortgage Loan Down Payment Goes Straight to Your Equity. Building up equity is a great idea because it means that you own more of your home. If you have equity in your home, you may qualify for a home equity loan or line of credit ("What You Should Know About Home Equity Lines of Credit").

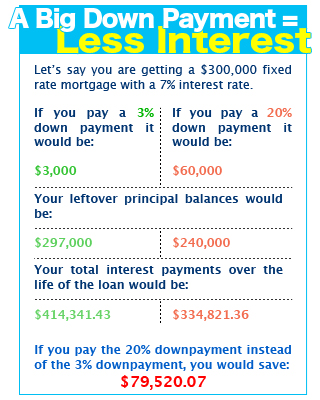

2. You Will Pay Less in Interest. When you take out a home mortgage loan, you are charged interest for the amount you borrow, which is the principal. Therefore, the more money you borrow, the more interest you have to pay. To reduce the amount of interest you have to pay, you can put down a larger down payment. Your down payment reduces your amount of principal. To see the difference your down payment makes in the amount of interest you have to pay on a home mortgage loan, look at the chart above. 3. Your Interest Rate Will be Lower. If you put down a large down payment, your interest rates will be lower (Quinn 106). As a result, it will cost you less to borrow the money. The less you put toward your down payment, the higher your interest rates will rise and the more expensive your loan will become. 4. You'll Pay Less PMI. Now that you know why you should pay as large of a down payment as possible, it is time to look at how your term length affects your home mortgage loan. To read the next step in our Home Mortgage Loan Guide, go to Step 5: Term Lengths for Home Mortgages. The Rest of Our Mortgage Guide: Mortgage Guide Introduction Step 1: Understanding Home Loan Lending Basics Step 2: Being Pre-Qualified and Pre-Approved for Home Loans Step 3: Choosing a Type of Mortgage Step 4: Down Payments and Your Home Mortgage Loan Step 5: Term Lengths for Home Mortgages Step 6: Closing Costs For Mortgage Loans Step 7: How Much Mortgage Loan Can You Afford © Copyright www.Finackle.com |